Health insurance is an essential part of maintaining well-being and financial security. Whether you are visiting a doctor, seeking medical treatment, or filling a prescription, your health insurance card serves as a vital tool in managing your healthcare expenses. Understanding how to read, use, and leverage your health insurance card effectively can save you time, money, and unnecessary stress. This article will break down the components of a health insurance card, explain how to use it efficiently, and provide tips for getting the most out of your insurance coverage.

Understanding the Key Components of a Health Insurance Card

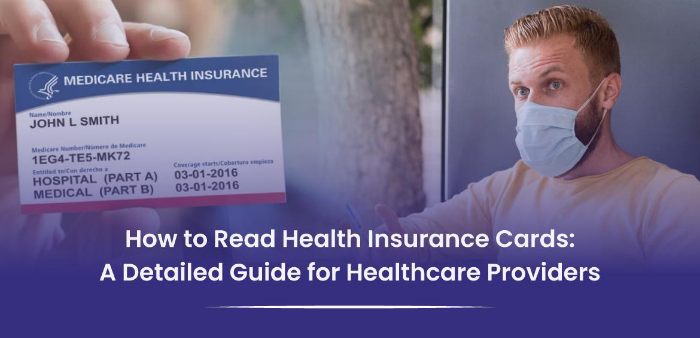

Your health insurance card is more than just a piece of plastic; it’s a valuable tool containing key information about your health coverage. Typically, a health insurance card includes several important details that both you and healthcare providers need to understand. Here’s a breakdown of the typical components of a health insurance card:

1. Member Information

- Member ID Number: This unique identifier is assigned to you by your insurance provider. It’s crucial for verifying your coverage, and it may be required when booking appointments or filling prescriptions.

- Member Name: Your full name, often listed alongside the primary policyholder’s name, if applicable.

- Group Number: If you have employer-sponsored insurance, the group number refers to your employer’s plan and helps identify it within the insurer’s system. This is important for claims processing and determining benefits.

2. Insurance Provider Information

- Insurance Company Name: The name of your health insurance provider (e.g., Blue Cross, United Healthcare, Aetna).

- Customer Service Number: This is the contact number for your insurance company. You can use it to inquire about benefits, find out about coverage, or resolve issues.

- Website Address: Many insurance cards include a link to the provider’s website, where you can access benefits information, find a doctor, or submit claims.

3. Plan Type and Network

- Plan Type: This refers to the type of health insurance plan you have, such as Health Maintenance Organization (HMO), Preferred Provider Organization (PPO), or Exclusive Provider Organization (EPO). Your plan type influences which healthcare providers you can see and how much you will pay for different services.

- Network Information: Your card may indicate whether you are covered for in-network or out-of-network providers. Understanding your network is crucial to avoid higher out-of-pocket costs.

4. Effective Date and Expiration Date

- Effective Date: This is the date your health insurance coverage starts. It’s important to know this, especially if you’re seeking medical treatment for something that may have been affected by your coverage period.

- Expiration Date: If applicable, this shows when your plan will expire and may need to be renewed or replaced. Some cards don’t include an expiration date, especially for long-term plans, but it’s always important to verify that your coverage remains valid.

5. Co-payment, Deductible, and Coinsurance Information

- Co-payment (Copay): This is the fixed amount you pay for certain services, such as a doctor’s visit or prescription, at the time of service. The amount is usually stated on your card.

- Deductible: The amount you need to pay out-of-pocket before your insurance plan starts covering your healthcare costs. Some insurance cards list the deductible amount, while others require you to check your benefits online.

- Coinsurance: The percentage of healthcare costs you share with your insurance company once your deductible has been met. For example, if your coinsurance is 20%, you will pay 20% of the cost of covered services, while your insurer pays 80%.

How to Use Your Health Insurance Card Effectively

Now that you understand the key components of your health insurance card, let’s explore how to use it effectively:

1. Carry Your Card with You at All Times

Always keep your health insurance card with you, especially when visiting healthcare providers or pharmacies. This ensures that you are prepared to provide your insurance details quickly when needed. Some insurers also offer digital cards via apps or websites, allowing you to access your card even if you don’t have the physical version with you.

2. Verify Your Information

Double-check that all the information on your health insurance card is correct. If you notice any discrepancies, such as incorrect member information or an outdated plan type, contact your insurance provider immediately to correct it. Accurate information is critical for proper claims processing and ensuring you don’t face unnecessary delays in receiving care.

3. Understand Your Plan’s Coverage

Familiarize yourself with your health insurance plan’s benefits, especially what is and isn’t covered. Your insurance card will often contain contact details and links to online portals where you can find detailed information about your plan. For instance:

- In-Network vs. Out-of-Network: If you have an HMO or PPO plan, it’s important to know which doctors or facilities are in-network. Visiting an out-of-network provider could result in much higher out-of-pocket costs, or your insurance may not cover the service at all.

- Specialist Referrals: Some plans, particularly HMO plans, may require referrals from a primary care physician (PCP) before seeing a specialist. Check your card for any specific instructions about referrals and follow them to avoid unnecessary charges.

- Emergency Care: Understanding how emergency care is covered, especially when seeking care out-of-network, can prevent unexpected costs. Most insurance plans provide full coverage for emergencies, regardless of the provider, but always verify this with your insurer.

4. Use the Customer Service Number

If you have questions about your coverage or need help understanding your benefits, don’t hesitate to call the customer service number listed on your card. Insurance companies can clarify any confusion about what services are covered, your copayments, deductible amounts, and even help with claims disputes. They can also guide you through the steps to find in-network providers or update your policy details if necessary.

5. Keep Track of Your Deductibles and Out-of-Pocket Maximums

Your insurance card may not always provide specific information about your deductible, out-of-pocket maximum, or coinsurance percentage. It’s important to keep track of these figures through your insurer’s website or app. Knowing your deductible is essential when planning medical procedures or visits, as it helps you understand how much you need to pay out of pocket before your insurer starts covering costs.

6. Review Your Insurance Card Regularly

Periodically review your health insurance card, especially if your insurer has made any changes to your plan. This is particularly important during annual enrollment periods when you might need to select new coverage options. If you switch jobs or insurance plans, you’ll receive a new card, and it’s vital to discard the old one to avoid confusion.

7. Know How to File a Claim

While many healthcare providers will file claims on your behalf, it’s important to know how to file one yourself if necessary. Some insurers require that you submit medical bills for reimbursement if you’ve paid out-of-pocket for covered services. Your health insurance card typically contains instructions on how to file claims, including contact information and the necessary forms to complete.

Tips for Saving Money with Your Health Insurance Card

To maximize the value of your insurance and avoid unnecessary costs, consider the following tips:

- Utilize Preventive Care: Many insurance plans cover preventive services at no additional cost. Be sure to take advantage of these services, such as annual check-ups, vaccinations, and screenings, to catch potential health issues early.

- Use In-Network Providers: Always choose in-network providers to save on costs. Out-of-network care often results in higher out-of-pocket expenses.

- Check for Discounts or Programs: Some insurance companies offer discounts for things like healthy lifestyles, smoking cessation programs, or weight management. Review your benefits to see if you qualify for any additional savings.

Conclusion

Your health insurance card is not just a small piece of plastic; it’s an essential tool that connects you to your healthcare coverage. Understanding the key components of your card, how to use it, and how to make the most of your insurance coverage can save you time and money. By regularly reviewing your plan, keeping track of your benefits, and staying informed about how your coverage works, you can navigate the healthcare system more confidently and effectively. Whether you’re seeing a doctor, filling a prescription, or seeking emergency care, using your health insurance card properly ensures that you are receiving the full benefit of your health plan.